A non-profit client used QuickBooks for its bookkeeping. The client had funds were invested in a brokerage account and wanted to be able to record dividend income, brokerage fees and unrealized gains or losses on the account in QuickBooks.

Tracking the individual stocks and mutual funds in QB wasn’t necessary for this client; the Board of Directors just wanted to be able to see the overall income and expenses in their monthly reports.

This could be done with either a journal entry or a zero-sum check, which will be shown here. A zero-sum check serves the same purpose as a journal entry, and, as the name states, has a total value of zero.

Here are the steps:

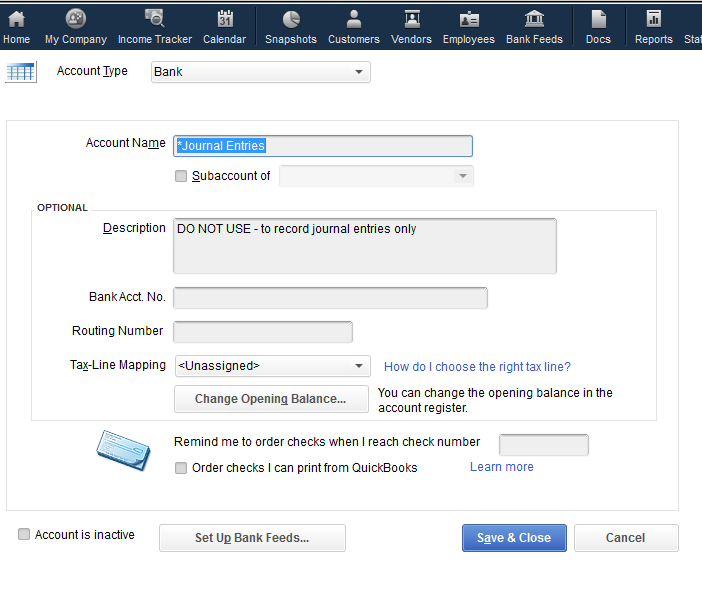

1. Create a new BANK type account named “Journal Entries,” which will be used as the account on which zero-sum checks are written and as the first line in — you guessed it — all journal entries.

2. Create an “Other Income” type account named “Unrealized Gains or (Losses)” and and “Other Expense” type account named “Brokerage Fees and Charges.”

3. Create a vendor to use on the checks. This will allow you to create reports by vendor. On our sample check, we used “Investment Income.”

4. Using the current month brokerage statement, determine the dividend income, brokerage fees, and unrealized gain or loss to the account, allocating each properly to the specific funds, if applicable. Our TEST Non-Profit Foundation has two funds that are sub-accounts under the “parent” brokerage account. Income and expenses are allocated by percentage to those sub-accounts.

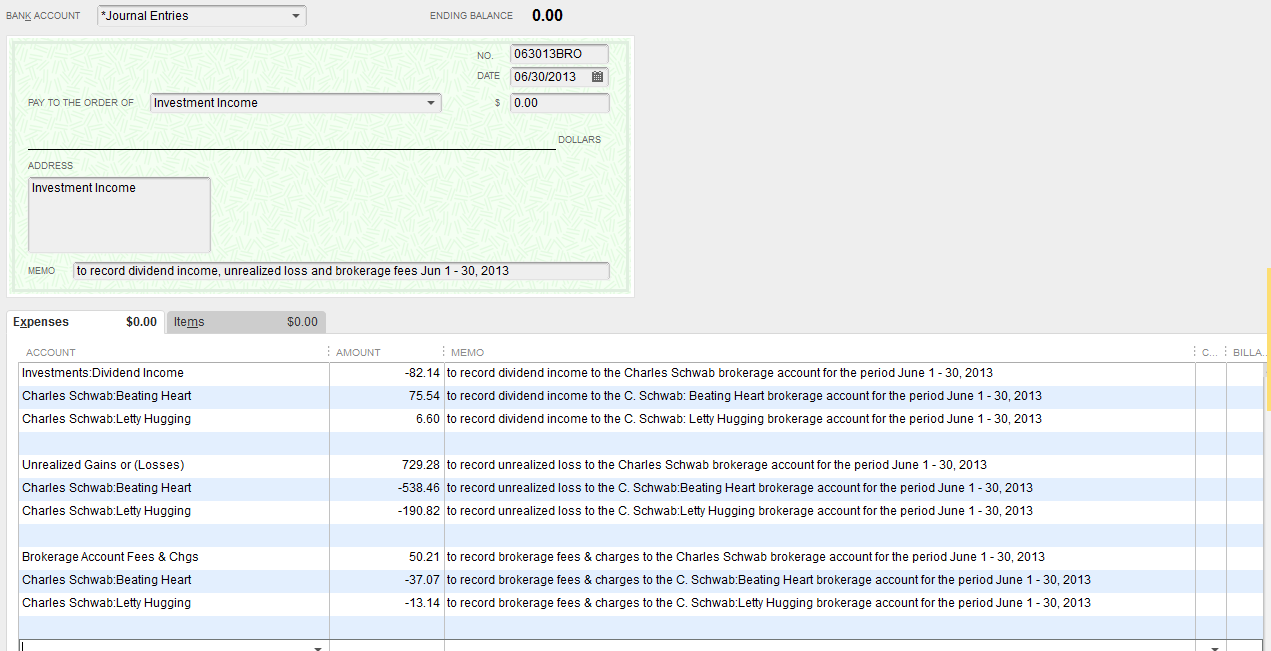

5. Go to BANKING> Write Checks. A check form will open. In the BANK ACCOUNT field at the top of the form, select the Journal Entries account. Enter a check number using any numbering system of your choice. Our sample check uses the date of the statement followed by BRO for brokerage. The amount will be 0.00.

6. On the EXPENSES tab on the “stub” section of the check, record the dividend income, Brokerage Fees, and Unrealized Gains or Losses, allocating the amounts to the various funds on the second line so that the amount “zeroes out.”

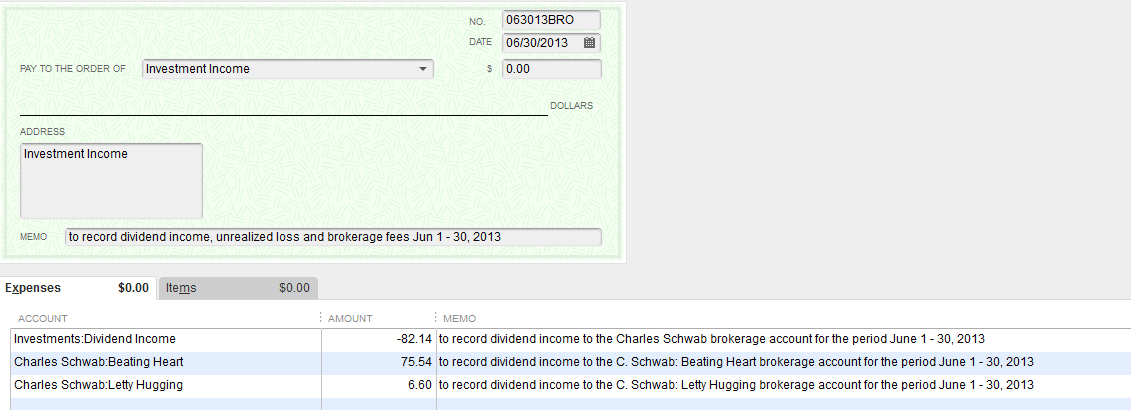

The graphic is a bit small so here is a close-up of the dividend income section:

Posting unrealized gains or losses can be a bit tricky, so here is a mnemonic to help:

The total amount of an unrealized gain is posted as a negative number of the “unrealized gain/loss” account (Other Income type account), and as (a) positive number(s) to the various sub-accounts that make up the brokerage account in the non-profit’s QuickBooks file. This increases the amounts in the sub-accounts.

The total amount of an unrealized loss is posted as a positive number to the “unrealized gain/loss” account and as negative numbers to the various brokerage sub-accounts. This lowers the amounts in the sub-accounts.

Nothing is posted to the “parent” brokerage account. Here is a close-up of that section of the zero-sum check stub:

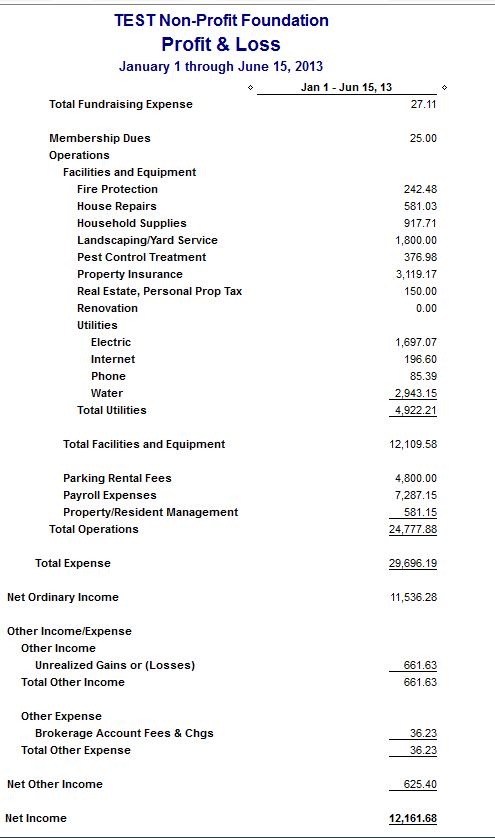

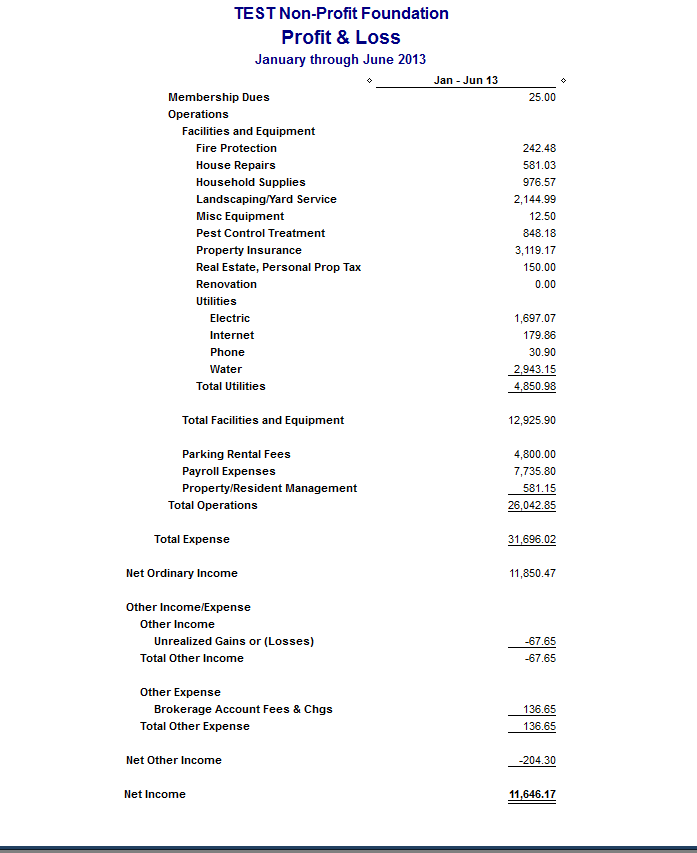

Running a Profit and Loss Report dated prior to the brokerage statement and after the brokerage statement shows the effect that the entries have on the “unrealized gains or losses” and “brokerage account fees and charges” accounts.

I hope this is helpful.

Wishing you a happy and prosperous day.

Patti Killelea-Almonte

Bookkeeping and Business Services